Here is why HDB prices have been falling for the last 5 years:

Do you feel a bit of heartache every time the news report that HDB prices are dropping? This has been happening for the past 5 years. This steady downtrend can be easily explained with 3 main reasons. Firstly, HDB has been supplying the market with nearly 10 times more BTO flats than a decade ago. Higher supply means lower prices.

Supply of new HDB flats is nearly 10 times higher today than the average a decade ago in the early 2000s.

HDB Motto is to fulfil dreams, build homes, and create communities. This is part of the reason why prices have been kept low.

HDB Motto is to fulfill dreams, build homes, and create communities. This is part of the reason why prices have been kept low.Lastly, tight regulations restricting when you can buy or sell HDB flats prevents prices from going up. These factors combined put heavy downward pressure on prices, and will continue to do so for the next decade or so. Would you want to avoid being trapped with a depreciating asset? Let us know! This is Isaac, keeping property real for you.

Private property market in Singapore can be tricky indeed. In our previous two posts, Part 1 and Part 2 of this series, we discussed possible factors that may cause private property prices in 2019 to stall. Today, we will discuss bullish factors for Singapore private property prices in 2019.

Singapore is one of the nicest places to live in

We all know that Singapore is one of the nicest countries to live in the world. Many foreigners come to our country and buy our properties because they recognise the value of our country’s security, stability and prosperity. However, it is our opinion that immigration trends would not be the biggest influence on prices in 2019.

Developers’ Land Cost is a big factor

Instead, one of the most influential factors on prices would be the developers in Singapore. Developers in Singapore acquire land either from the government through government land sale (GLS) or from collective sales (en bloc). Subsequently, after building on the land, developers will then sell it to property buyers like you and I at a profit. As such, the price at which developers obtain their land bank would be a huge factor in determining the eventual private property price sold to the average buyer. This is because land cost is the developers’ single largest cost in their business.

Record-breaking land sales in 2017 to 2018

In year 2014 to 2016, there were a total of 33 land sales, comprising 29 government land sales and 4 en blocs. However, in 2017, a frenzy for enbloc sale across the country started. In just this one year alone, developers snapped up land in 37 land sales which was valued at $8.65 billion. That is more than the previous 3 years combined. Moreover, in the first half of 2018, the craze continued and 43 land sales totalling $10.1 billion worth of land was added to developers’ bank. The combined value of these one and a half year is almost double of the record setting year of 2007, where 111 land sales valued at $11.3 billion was acquired by developers.

Record-breaking Land Costs = Record-breaking Property Prices?

That is a lot of numbers, but the implication is this.

Property prices rebounded sharply and quickly in 2008 because the rush of en bloc money flooded the property market.

Notice that in 2007, despite the recession caused by the subprime crisis, property prices rebounded sharply and quickly. This was because the rush of en bloc money flooded the property market with cash rich buyers that needed new places to stay after their homes were collectively bought out. We are seeing a similar circumstance today. The combined $19 billion purchased at record-breaking cost to developers will definitely have an impact on prices in the years to come, even if it is beyond 2019.

In summary, with all the factors presented to you so far, it is up to you to eventually decide which factors will play the most important role in determining prices, be it up or down. We find that the best way to add value as property agents is to provide our carefully-researched perspective and then advise you accordingly, so we hope that you have benefited from this series. If you like our approach and would like to benefit from our quantitative analysis as well, feel free to contact us and we will do our best to provide our best service. That’s it for today, this is Isaac, keeping property real for you.

If you enjoy this post, please subscribe to our Youtube channel and click on the bell icon to keep notified of our new content! You can also comment below to let us know what topic you want us to cover!

Prices in a market reflect the meeting point of supply and demand. Since we are not fortune tellers, there is no way for us to definitely pinpoint the extent of price movement in Singapore’s property market. What we seek to do is to analyse factors affecting broader housing demand and supply. We did so in part 1 of our series. Hopefully, part 2 will continue to allow you to make a much more informed conclusion. With that in mind, let us continue our analysis of private property market in 2019.

Population growth is limited

First of all, let us not forget that a large part of our housing demand is contributed by new citizens.

We have about 4 million resident Singaporeans that can contribute to housing demand.

With a total of about 4 million resident Singaporeans, we should note this group as the main demand contributor. While non-residents will most likely only rent, resident Singaporeans are much more likely to purchase properties in Singapore. It is common knowledge that Singaporeans are not the best at making babies.

Low Total Fertility Rate has been prevalent for the past decade, which means unlikely growth in population from natural births.

This can be seen from our low fertility rate. This means that we cannot count on a boom in population from Singaporeans as a sudden demand factor for housing.

Immigration figures were kept low for the past decades due to concerns from locals about capacity issues.

In addition, if we look at immigration figures, the number of new citizens has remained large flat since 2010. This leads us to conclude that we cannot expect demand growth if we are looking at population or immigration growth alone.

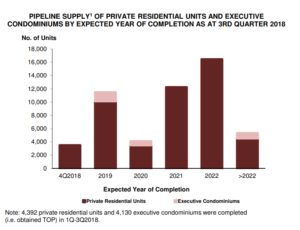

Large supply incoming

Next, let’s look at another key determining factor for property prices: supply. Few years ago, developers were aggressively acquiring land to build private properties.

Private property pipeline supply figures provided by URA clearly shows a large glut of private properties headed our way in the coming few years.

Many of these projects are expected to be completed within the next few years, and we can see this clearly from pipeline supply figures provided by URA. This will add to an already wide variety of choices that buyers can choose from, which will apply downward pressure to prices. Of course, we also have to recognise that property is not a commodity and buyers will still pay a premium for good properties. There is still value even in a well-supplied market- we just have to look a lot harder.

Regulations can be removed to boost demand

It is not all doom and gloom for Singapore property market of course. There are certain factors that will prop up property prices as well. One of the most obvious factors that we know will prevent a crash in property prices is the numerous restrictions on property buyers. This prevents reckless speculation that destabilises property markets. More importantly, in the event of a downturn, the government can remove some, if not all, of these regulations. That will almost definitely cause a spike in demand. In our final video up next, we will discuss other bullish factors for Singapore private properties. Stay tuned! This is Isaac, keeping property real for you.

In Singapore’s short history, some people became millionaires by timing the property market correctly. Yet there were also many more people who have lost entire fortunes by entering the property market at the wrong time. In one of the previous insights that we shared, we mentioned that the long-term property trend is going up.

However, there is also a saying that the market can stay irrational longer than you can stay solvent. This means that if one cannot survive the short-term volatility, they will not be able to see the fruits of their labour. In our special three-part video series, we will discuss where we think the Singapore property market will head towards in year 2019. In summary, it is our view that there is more short-term downside ahead for Singapore private property prices.

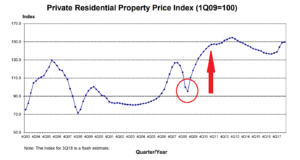

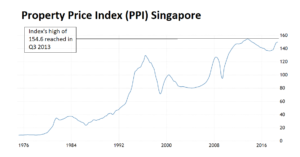

Prices nearing all time highs

Firstly, we need to recognise that prices are nearing an all-time high.

Property prices are nearing all time high in Singapore which is evident from Property Price Index (PPI)

We can see this from the PPI, and this is a price level of huge significance. It is much harder to break through an all-time high price. The logic is this: If you are a buyer who purchased a private property at a high in 2013, you would have been sitting on a loss for 5 agonising years. When property prices finally catch up to your breakeven price, you would be more inclined to sell. This will increase the supply of private property on the resale market.

At the same time, if prices are at an all-time high, the pool of buyers will also decrease because not many buyers will dare to buy their private properties at an all-time high. With larger supply and lower demand, it explains why prices tend to reject from prior highs. However, this point is under the assumption that there are no other sudden demand factors.

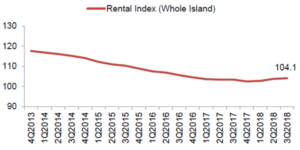

Soft rental market for past 5 years

The next point is that rentals have been mostly flat for the past 5 years.

Rentals have been falling and staying low for the past few years and do not look set to bounce within the foreseeable future, from the Rental Price Index (RPI).

There are many property investors that take up mortgages to purchases multiple properties. This is done with the intention of renting them out. The rent collected is then used to pay the monthly instalments on the mortgages. With falling rentals, it will become harder to sustain such a method of property investment. This means that some of such property investors may be forced to offload their properties if and when they are unable to find tenants at a sustainable rental price. Less people will also adopt such a method of property investing when they see that the prevailing rentals are unsustainable. In short, lower demand and higher supply again.

Rising Interest Rates

The last point we will make in this video is the most important one that significantly affects property purchase decisions. Interest rates in Singapore, known as Singapore Interbank Offered Rate, have been going up and will continue to go up in the near future.

SIBOR looks set to go up in tandem with US Federal Funds Rate.

SIBOR is closely correlated to the U.S Federal Funds rate, which will has been indicated to rise in the coming years.

With higher interest rates, less people will be able to afford the more expensive monthly repayments. Overleveraged property owners will also find it harder to refinance when their lock-in period expires. Many of such property owners who took too many loans will be forced to sell off their properties. This happens when they are unable to keep up with the higher interest rates. The situation will be worsened if they are unable to find tenants to rent out their properties as mentioned previously.

In the next post, we will discuss two other factors that may further drive down property prices in Singapore. Till next time! This is Isaac, keeping property real for you. If you enjoy the explainer video, please subscribe to our Youtube channel and click on the bell icon to keep notified of our new content!

Here is where Singapore property prices are headed to in the long run:

Every family gathering, you always seem to hear your talentless but rich relative bragging about his numerous private properties. You are silently angry about the unfairness of the world. Yet, you are also wondering to yourself if it is already too late for you to enter the fray. After all, property prices have already risen by so much. Surely this means that what goes up must come down soon? However, it will be foolish to try to predict the market without looking at solid facts and figures. So let me share with you my perspective.

Everything is related!

Before we begin analysing the Singapore property market, the first important point to note that the economy, the stock market, and the property market are correlated to one another. Without boring you with too much details, this could be because they are all affected by the same factors such as interest rates, investors’ confidence, and political stability. However, we must be clear that correlation does not equal causation. For example, if I see a pretty girl every single time that I eat at the coffeeshop opposite my house, it does not mean that my presence causes pretty girls to appear. In the same way, the trend of the economy, the stock market and the property market was not caused by one another.

We first take a look at the bread and butter of Singapore’s property market – HDB flats. HDB’s Resale Price Index (RPI) tracks the price movement of HDB flats over the past few decades, and there has clearly been an uptrend in prices.

HDB Resale Price Index indicating a long term uptrend in prices.

This is an indication that Singaporeans generally believe in the fundamental strength of the property market, which with an increasing population, more Singaporeans are buying property than selling through the years. However, notice that there is a slowdown in HDB flats prices recently.

HDB RPI shows that the previous slowdown lasted 15 years, and the current pause in prices has only been for less than 8 years.

This could be because of the large numbers of Built-To-Order, or BTO, flats that has been released in recent years. The previous pause in prices lasted about 15 years, and as of today at 2018, the pause in upswing of HDB prices has lasted less than 8 years. It is likely that HDB prices will stay stagnant in the near future.

Private Property market outlook

Next, we turn to the Property Price Index of private properties in Singapore, released by URA.

Private property prices have also been on longterm uptrend, and pauses in uptrend last for less than 5 years.

Again, we see an uptrend. This time round, it is quite clear that the private property market is headed up more strongly than HDB prices. Even previous pauses in price lasted less than 5 years. This could be because private properties like condominiums can be readily bought by foreigners with no restrictions, unlike HDB flats that can only be bought by Singaporeans. In addition, it is also much easier to rent out private properties than HDB flats. This means that for an investor, private properties seem to be a more attractive option.

The trend is your friend, until it ends!

In conclusion, while we cannot predict the future, we can form a view and forecast based on current trends. The strong long term uptrend in Singapore private property prices tells us that Singapore properties are being highly valued. As such, one of the greatest investment advice that I can offer you is that the trend is your friend, until it ends. I hope you have gained some insights, and that’s it for today! This is Isaac, keeping property real for you.

Of course, it’s easier to spot long term trends. How about short term trends? Find out our outlook for Singapore private property market in 2019 here!

Considering to buy a new property? Find out how you can better prepare yourself here!

If you like our content, be sure to like, comment on the video and subscribe to our Youtube channel. You can also bookmark our page!

Did you just start a family and are looking forward to purchasing your new home? Or looking to buy a property for investment purposes? One of the most important questions that you would be asking would be whether to buy a leasehold or a freehold property. The answer depends if you are planning to buy the property to stay in or to invest in.

Freehold is not really freehold

Even for investment, many people will prefer freehold properties. Most Singaporeans believe that this means that they can own the property forever. However, in Singapore, there is the Land Acquisition Act, which means that even a supposed freehold property can be taken by the government. This is usually done in the name of public interest such as to build MRT or expressways. Indeed, you may technically hold a freehold estate forever. However, the building itself will need constant upgrading and renovations at some point. This is to prevent it from falling apart and this will eat into your expenses if you are not mindful. Next, freehold estates usually cost 10% to 15% more than a leasehold estate that is similar in size. This higher capital outlay that will result in higher monthly repayments.

High Initial Capital Outlay = Lower Rental Yield

Moreover, if you’re intending to rent out the property, tenants don’t care if the property is leasehold or freehold. They are more likely to care about the location or the amenities available in the area. Because of higher capital outlay for freehold property, it follows that the rental yield will be lower for freehold properties. This is in comparison to leasehold properties in the same location. As such, capital appreciation of leasehold property in central region of Singapore tends to be even higher than the capital appreciation of a freehold property outside of central region, like say in Yishun or in Pasir Ris.

Advantage of freehold properties

On the other hand, freehold properties hold an advantage when it comes to taking loans/using CPF. There are many restrictions put in place when taking loans for leasehold properties. This is especially so for older leasehold properties that freehold properties are not subjected to.

It all boils down to what you need

In summary, leasehold properties may be the better option for investment purposes. If you want to buy the property to stay in, both options are viable depending on your needs. We need to always ask ourselves what our purpose is, then make an informed decision from there. That’s it for today! This is Isaac, keeping property real!

Not sure if you should even be buying a property for long term investment? Check out our analysis on the long term outlook for property market!

If you like our content, be sure to like, share, or comment on the video and subscribe to our Youtube channel. You can also bookmark our page!